The Department of the Treasury (Treasury) has released a final rule imposing restrictions on U.S. outbound investment in Chinese companies active in developing certain national security technologies (Final Outbound Rule).

The rule, which was released on October 28, 2024, and takes effect on January 2, 2025, imposes additional diligence responsibilities, record-keeping and notification requirements, and restrictions on U.S. persons and their controlled foreign entities engaging in certain transactions with foreign persons in “countries of concern” (currently limited to China) that perform defined activities related to semiconductors and microelectronics, quantum information technologies or artificial intelligence (AI) (together, “sensitive sectors”).

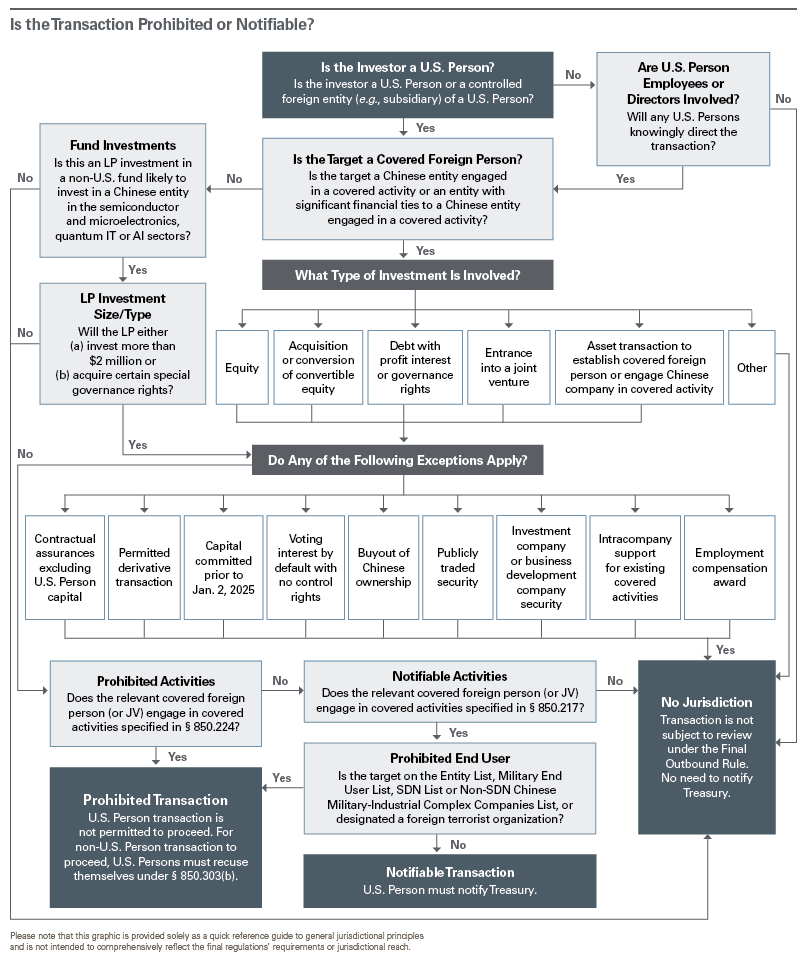

Unlike the Committee on Foreign Investment in the United States (CFIUS), the Final Outbound Rule — which has been referred to as a “reverse CFIUS” program — does not create a transaction-specific screening and review mechanism.

Instead, it outsources the primary regulatory compliance burden to the relevant U.S. investor or investment management professional.

As shown in the chart below, the Final Outbound Rule requires U.S. citizens, lawful permanent residents and entities (including limited partners, or LPs, and U.S. individuals serving in key management roles in non-U.S. entities) (together, “U.S. Persons”) to notify, abstain from or take action to prohibit certain transactions (“covered transactions”) related to Chinese companies or related companies engaged in specified activities in sensitive sectors (“covered activities”). (Companies engaged in covered activities are “covered foreign persons.”)

Below, we highlight key features of the Final Outbound Rule with the not-insignificant caveat that because this rule is not based on legislation, the incoming Trump administration will be free to modify or withdraw the rule. Given that at least some Republican members of Congress have already criticized the rules as inadequate, we expect the Trump administration will be inclined to give these rules a very hard look.

Covered Transactions

The Final Outbound Rule applies to the following types of investment or investment-related transactions (both direct and indirect):

- acquisition of equity or a contingent equity interest,

- provision of certain debt financing,

- conversion of contingent equity interest into equity interest,

- involvement in greenfield or brownfield investment,

- entrance into a joint venture, or

- acquisition of a limited partner interest in non-U.S. fund.

Whether a transaction is a covered transaction depends on whether the U.S. Person has “knowledge” at the time of the transaction, to include undertaking “a reasonable and diligent inquiry,” that a specific transaction is a covered transaction — i.e., whether the transaction involves a covered foreign person engaging in a covered activity.

The Final Outbound Rule places ongoing notification requirements on U.S. Persons if a U.S. Person learns after closing that the transaction was a “covered transaction,” putting a spotlight on the adequacy of any pretransaction diligence.

While obtaining representations and warranties is a factor in satisfying the “reasonable and diligent inquiry” standard, this factor is not dispositive, nor does the Treasury Department identify specific representations or warranties that would be sufficient to meet this requirement.

Rather, the Final Outbound Rule suggests that a more individualized review may be required. It does so by identifying a noninclusive list of factors such as diligence questions asked of a target, analysis of publicly available information, the presence of “warning signs” such as evasive diligence responses and efforts to obtain nonpublic information relevant to transaction, as relevant to determining whether a U.S. Person had “knowledge” the transaction was a “covered transaction.”

The Final Outbound Rule includes some exceptions and safe harbors for transactions that do not typically provide investment targets with the type of intangible benefits of U.S. Person investments that the Final Outbound Rule was designed to regulate.

For example, the rule exempts the acquisition of publicly traded securities, as well as passive U.S. LP investments into non-U.S. funds below $2 million (or where the LP obtains contractual guarantees that its capital will not be used in a prohibited/notifiable transaction). The Final Outbound Rule also exempts some intracompany transactions between a U.S. Person parent and its subsidiary that may otherwise be a covered foreign person, as well as certain debt and derivative transactions.

Additionally, most agreements entered into prior to January 2, 2025, are not captured, although any subsequent, related transactions on or after January 2, 2025, would need to be carefully reviewed under the Final Outbound Rule.

Covered Foreign Persons

The Final Outbound Rule defines “covered foreign persons” to include any person or entity that “engages in” a covered activity who is:

- a citizen or permanent resident of China and not a U.S. citizen or permanent resident,

- (if an entity) headquartered or with its principal place of business in China, or incorporated or organized under Chinese law,

- a Chinese government party, or

- any entity, wherever located, where 50% or greater voting interests, board interests or equity interests are held by persons described above (“persons of a country of concern”).

The term also includes any person, including U.S. Persons, who holds certain equity, voting or governance interests in a covered foreign person, from which such person derives a majority of their income or incurs a majority of their expenditures or expenses (e.g., variable interest entities).

Thus, U.S. Persons must look beyond investments in China to transactions with covered foreign persons in third countries and must also consider whether their investments may be used to establish a covered foreign person. U.S. investors will need to ensure that their investments into non-Chinese targets in sensitive sectors do not inadvertently create an indirect notifiable or prohibited transaction.

Moreover, because the Final Outbound Rule does not set a de minimis level of activity that would qualify as “engag[ing] in a covered activity,” determining whether a person of a country of concern “engages in” a covered activity is likely to be a key diligence challenge.

Notifiable and Prohibited Transactions

The Final Outbound Rule defines two different classes of covered transactions — notifiable transactions and prohibited transactions — based on the type of activity in a sensitive sector in which a covered foreign person engages. (See table below.)

An obligation to notify the Treasury Department of a transaction is triggered where a covered foreign person engages in:

- designing, fabricating or packaging integrated circuits (ICs) (where the transaction is not a prohibited transaction), or

- developing AI systems (1) designed for military or government intelligence or mass surveillance uses, (2) intended to be used for cybersecurity applications, digital forensics, penetration testing or control of robotic systems, or (3) trained using a defined threshold of computing power.

A transaction is prohibited if it involves sensitive sector activities implicating:

- certain advanced technologies (i.e., those technologies exceeding certain performance or power thresholds) or military or intelligence end uses, or

- foundational and related technology (design software for ICs, developing or producing semiconductor fabrication or packaging equipment, and a range of actions related to quantum computing and related activities).

Covered activities include research and initial development or design work as well as modification and certain testing activities.

Further complicating an investor’s diligence burden, even an entity that outsources these activities can be considered “engaging in” the covered activity in addition to making the third-party entity providing those services a potential covered foreign person.

Activities by US Persons in Non-US Companies

Although the obligations in the Final Outbound Rule extend to U.S. Persons, they can impact non-U.S. funds and other companies in several ways.

For example, a U.S. Person must take “all reasonable steps” to ensure their controlled (i.e., greater than 50% voting interest) foreign subsidiaries (“controlled foreign entity”) do not engage in prohibited transactions and must report notifiable transactions by their controlled foreign subsidiaries. A U.S. Person who holds certain executive functions at a foreign entity but is not otherwise a “parent” of the entity must not “knowingly direct” a transaction that would be a prohibited transaction if engaged in by a U.S. Person.

The Final Outbound Rule provides safe harbor to such U.S. Persons who recuse themselves from certain decision-making activities with respect to the would-be covered transaction.

Finally, passive U.S. LPs investing more than $2 million will have diligence requirements when investing in foreign funds and in certain circumstances must obtain contractual assurances that the non-U.S. fund will not engage in covered transactions.

Penalties

The Final Outbound Rule does not establish independent penalties but relies more broadly on penalty amounts authorized under the International Emergency Economic Powers Act, similar to the penalties available under economic sanctions programs administered by Treasury’s Office of Foreign Assets Control.

Civil penalties can be imposed to the greater of either $250,000 (adjusted for inflation, currently $368,136) or twice the value of the transaction that serves as the basis of the violation.

Persons who willfully violate the Final Outbound Rule may be subject to a fine of up to $1 million and be imprisoned for up to 20 years.

The secretary of the Treasury can also take actions to require divestment for any prohibited transaction. Where an investor believes a violation may have occurred, they may submit a voluntary self-disclosure to Treasury that will be taken into account in assessing any penalties.

A More Complicated US Regulatory Landscape

The thresholds and covered activities established in the Final Outbound Rule complement, and were informed by, adjacent U.S. regulatory regimes, but do not perfectly match them.

For example, technical thresholds in the Final Outbound Rule are not a perfect match to technical thresholds established in the Export Administration Regulations or International Traffic in Arms Regulations for ICs and related hardware.

Covered activities are also not a perfect match to activities associated with a “critical technology U.S. business” under the CFIUS regulations, and the Final Outbound Rule covers a much broader set of transactions than those regulated by CFIUS.

While the Final Outbound Rule does make some effort to conform definitions with some other national security regulatory regimes (e.g., the definition of “AI system” with Executive Order 14110, on the “Safe, Secure and Trustworthy Development and Use of Artificial Intelligence”), investors will need to carefully analyze the Final Outbound Rule’s definitions against a prospective target’s technology to determine applicability.

Takeaways

The Final Outbound Rule is broad in capturing U.S. Persons, wherever located, and in defining covered foreign persons to include their subsidiaries abroad and those with significant financial relationships. But the rule is limited in that it narrowly tailors the scope of covered activities to defined activities within sensitive sectors.

We expect that the Final Outbound Rule may have a limited impact on investments and related transactions, due in part to the de-risking in relevant Chinese markets already being undertaken by U.S. investors and tech companies in response to current and anticipated U.S. regulatory restrictions.

They include:

- Reporting requirements and restrictions in relation to the Commerce Department’s Information and Communications Technology and Services regulations.

- Mitigation restrictions as a result of receiving CHIPS Act funding.

- Risk factors for CFIUS and ex-U.S. foreign direct investment screening regimes.

- Export controls on semiconductor, AI and quantum computing-related hardware and technology.

- Forthcoming regulations such as a rule restricting access to U.S. bulk data.

All together, these new and anticipated regulatory regimes will work to restrict or prohibit U.S. Person involvement in sensitive sectors in China and any other country of concern that the U.S. president may name.

Nonetheless, the Final Outbound Rule may impose significant diligence and related compliance obligations, directly or indirectly, on U.S. investors, U.S. companies engaging in cross-border transactions implicating the sensitive sectors and similarly situated non-U.S. firms with U.S. management personnel.

The Final Outbound Rule may not be the last word on regulating U.S. outbound investment. As noted in the rule, several pending bills in Congress could supersede portions of the Final Outbound Rule. Moreover, and as previously noted, the incoming Trump administration may expand the scope of the restrictions or otherwise change the rule.

Additionally, the U.S. may not be alone for long in imposing such restrictions. The European Commission has expressed some interest in exploring parallel outbound restrictions for European Union investors — though there appears to be much less appetite for pursuing them than has been the case in the U.S.

| COVERED ACTIVITIES | ||

|---|---|---|

| SECTOR | PROHIBITED | NOTIFIABLE |

| Semiconductors and Microelectronics |

Development or production of:

Design or fabrication of:

Development, installation, sale or production of certain supercomputers enabled by advanced ICs. |

Design, fabrication or packaging of ICs not otherwise covered in "prohibited" category. |

| Quantum Technologies |

Development of quantum computers or production of any critical components required to produce a quantum computer. Development or production of:

|

N/A |

| AI |

Development of any AI system:

|

Development of any AI system not otherwise covered by the prohibited transaction definition, where such AI system is:

|

This memorandum is provided by Skadden, Arps, Slate, Meagher & Flom LLP and its affiliates for educational and informational purposes only and is not intended and should not be construed as legal advice. This memorandum is considered advertising under applicable state laws.